Read Time: 4 minutes

“I know investing is important, but which one should I invest in?”

If this is you, you’re not alone.

It is normal to feel lost when learning how to invest.

Because it’s not like we are taught in school on different types of investments we can choose.

In this week’s newsletter, I’ll share with you 7 DIY investment options you can consider to invest in.

Disclaimer: Any investment mentioned below is for educational purposes, not investment advice. Please do your own due diligence before investing in any asset.

1/ Amanah Saham (ASNB)

Risk: Low to Medium

Amanah Saham is an investment exclusively for Malaysians. You won’t see this info from US-based financial content.

There are 2 types of ASNB investments: fixed-price funds and variable-price funds.

Fixed-price funds are the underrated investment that most Malaysians should consider. As the fund unit is fixed in price, it is unlikely for investors to lose money due to capital.

Moreover, their returns are better than fixed deposits.

Meanwhile, variable-price funds are similar to unit trusts, which I will cover later.

2/ Stocks

Risk: High

Stock is the mainstream investment that everyone talks about. Each stock represents a company, and its price is determined by the stock market sentiments.

Market sentiment refers to the overall attitude of investors toward a particular security (in this case, stock) or market.

There are 2 ways you can profit from your stock investment:

- Capital gain: when your stock price goes up

- Dividends: a cash payout by companies to shareholders, like interests from banks

Here are 5 stock categories that you may want to know:

- Dividend Stocks: Stocks that give high dividend yield (>4%).

- Growth Stocks: Stocks with high growth in revenue and earnings.

- Value Stocks: Stocks that appear lower price relative to its revenue and earnings.

- Blue Chip Stocks: In Malaysia, they are the top 30 largest capital stocks in KLCI.

- Penny Stocks: Stocks that are dirt cheap (less than RM1 per unit), favored by traders.

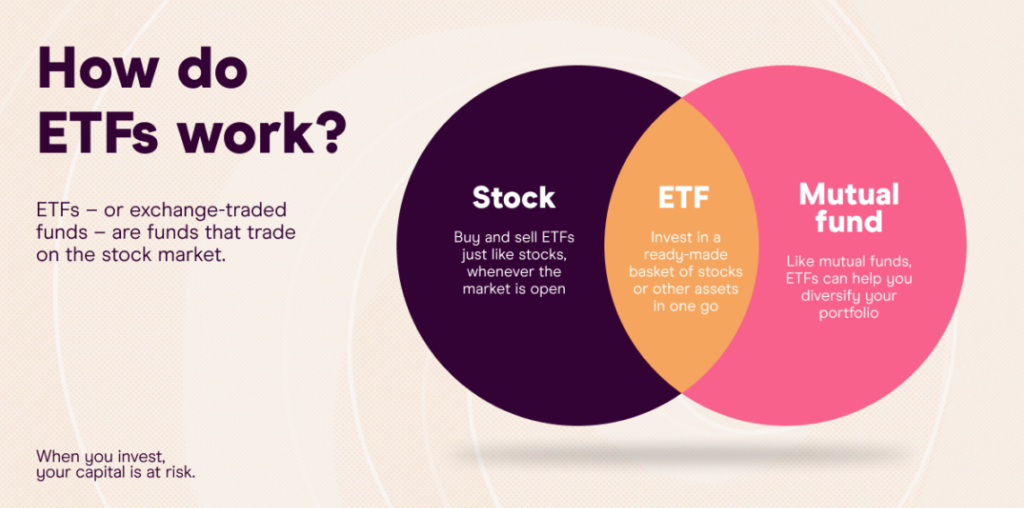

3/ ETF (Exchange Traded Fund)

Risk: Medium to High

Image Source: freetrade.io

An ETF is a type of fund that is traded like a stock but diversified like a unit trust.

There are a few types of ETF such as Index, commodity and industry.

Among all the ETF types, index fund ETF is the most popular one as they are well diversified and have more predictable returns. If you own an ETF that tracks S&P 500, your money is diversified into top 500 US companies tracked by S&P 500.

For more info about ETF, check out my Twitter thread:

4/ Unit Trusts/Mutual Funds

Risk: High

In Malaysia, we are more familiar with the term “unit trusts”. But in the US, they have more “mutual funds”. Both of them are very similar with a slight difference.

Basically, these are funds that are actively managed by fund managers. The money invested in the funds will be used by them to invest in stocks or ETFs.

Different unit trusts will have different portfolios of stocks/ETFs, depending on the purpose of the funds.

Since they are actively managed, there are annual fees that investors need to pay to the unit trust managers. This is how the banks earn money from you.

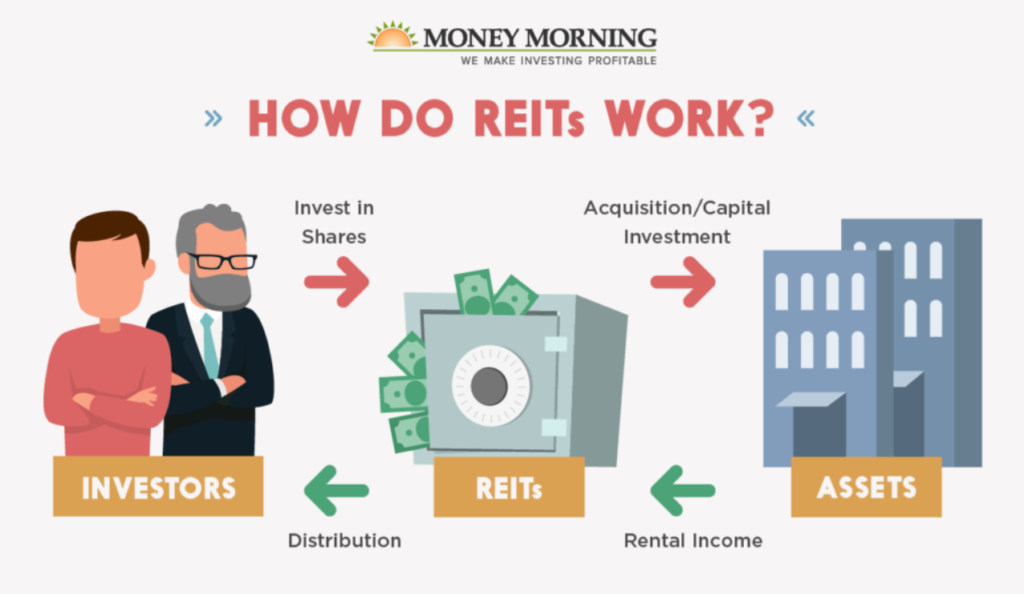

5/ REIT (Real Estate Investment Trust)

Risk: Medium

Image Source: MoneyMorning

A REIT is similar to a unit trust, but traded like a stock. You can think of it as a unit trust company that focuses on investing in properties.

Investing in REITs is a good way to have exposure in the properties segment. It is also a good alternative to property investing as you get to collect “rents” from properties, but in dividend form (or we call it income distribution)

The income distribution from REITs is subjected to a 10% pre-tax. Investors don’t have to declare the tax as it will be declared by REIT companies.

6/ Fixed Deposits

Risk: Low

This is probably the first investment for many Malaysians. Fixed deposits are products by banks that guarantee a return for your money deposited into it. In exchange, your money is locked with a period of time.

Good things about fixed deposits? It is a low-risk investment that comes with guaranteed return and is usually insured by PIDM.

The only disadvantage of fixed deposit is the penalty on early withdrawal. If you withdraw before the maturity date, you will get back your invested money without any interest earned.

7/ Money Market Funds

Risk: Low

Money market funds are a good alternative for fixed deposits. The main difference is MMF does not have a locked-in period that will forfeit your interests. Its flexibility is ideal for many investors to put their emergency fund in this investment to earn some extra cash.

Although the returns of MMF and FD are similar, MMF does not have guaranteed return and is not insured by PIDM.

Verdict

You may wonder, “is that all? I thought there are many more investments such as property, crypto, gold, bonds, equity crowdfunding, P2P lending, stock options, warrants, futures”.

Well, I purposely exclude them. It’s either they are high-risk investments or I’m not interested in explaining them.

If you are interested to know about them, let me know by comment below.

p/s: This week’s newsletter topic is inspired by my favorite blogger, Aaron, for his well-written article on DIY investment options in Malaysia on Mr-Stingy.

That’s all for this week, my friend!

Talk with you again next week.

Your Money Buddy,

Marcus

Whenever you’re ready, there are 2 ways I can help you:

1) Book a 1-to-1 Call Session with me to pick my brain, whether it is on investing, money management or any topic you would like to learn from me.

2) If you’re not sure which platform to invest your money, here are 3 platforms that I personally use:

→ Rakuten Trade – Where I invest in US index fund ETFs. Get RM30 worth of RT points if you register & unlock foreign trading with my referral link.

→ Wahed Invest – Where I invest in Shariah-compliant US ETF. Get free RM10 if you register a new account with my referral code “markeo1”

→ Versa – Where I invest my emergency fund with 4% return (until Aug 2023). Get free RM10 if you register a new account with my referral code “AL9JZJ9H”